You've worked for decades. You've saved diligently, contributed to your 401(k), and maybe even worked with an advisor. By most measures, you've done the right things.

Then retirement arrives, and the market drops. That's one of the biggest fears pre-retirees live with as they transition to retirement. It's also one of the most consequential risks in retirement planning, and it has a name: sequence of returns risk.

Sequence of returns risk refers to the timing of investment losses, not just their size. A market decline early in retirement, if you're not prepared, can significantly derail your retirement plan.

Most retirement plans focus on how much you've saved and what your portfolio might average over time. But averages can be misleading. A portfolio that averages 7% annually over 30 years doesn't earn 7% every single year. Some years are up 20%. Some are down 30%. And in retirement, the order of those up and down years matters enormously.

When you're still working and accumulating wealth, a market downturn is painful, but recoverable. The old saying goes, "It's a recession if your neighbor lost their job. It's a depression if you lost yours." The point is, when you're working, your income pays your living expenses.

At retirement, it's your investment portfolio that's working for you. Returns fund your future income, and you're now withdrawing from your portfolio to cover living expenses. You've probably heard the phrase, "Buy low, sell high." If you're not prepared, a downturn forces you to sell at a low price. Once sold, those shares are gone. They can't recover with the market. And the portfolio you have left is now smaller, meaning future withdrawals represent a larger percentage of a diminished base.

In plain terms: bad returns early in retirement are far more damaging than bad returns later, even if long-term average returns end up being identical.

If you're within five to ten years of retirement and haven't specifically addressed sequence of returns risk, now is the time to do so. The market will not wait for you to schedule a meeting.

Meet SamuelWhy This Matters for Retirees

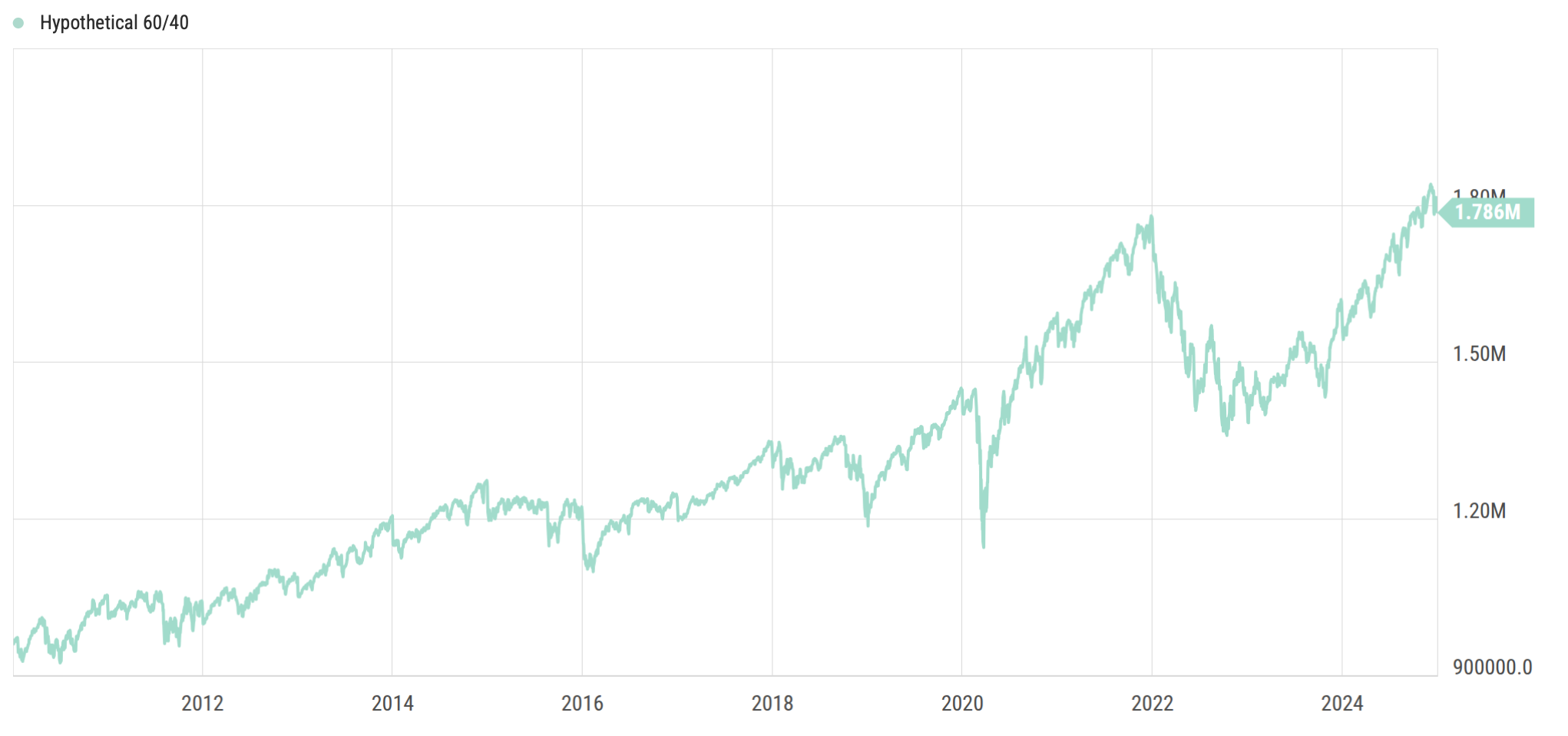

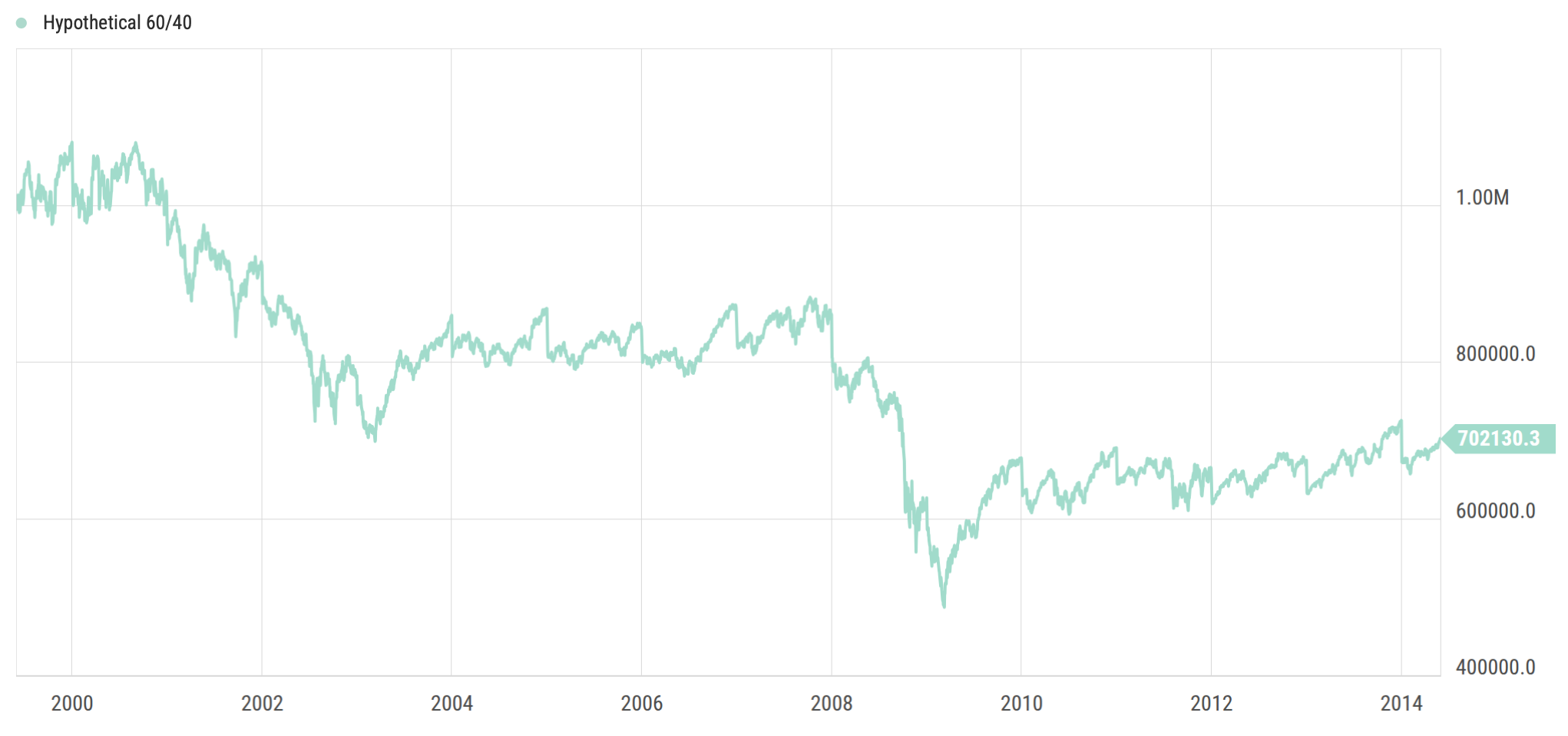

Consider two retirees, Margaret and Robert, who each retire with $1,000,000 and plan to withdraw $50,000 per year.

Margaret retires into a strong bull market in her first decade. Returns are solid early on, and her portfolio grows even as she draws income. By the time a rough stretch arrives later, her portfolio is large enough to absorb it.

Margaret's Portfolio (Jan. 2010 – Jan. 2025). Hypothetical portfolio beginning at $1,000,000 with $50,000 in annual withdrawals, allocated 60% S&P 500 (^SPX) and 40% Bloomberg U.S. Aggregate Bond Index (^BBUSATR). For illustrative purposes only. Indices are unmanaged and cannot be invested in directly. Past performance does not guarantee future results.

Robert retires into a bear market. He experiences a significant decline in years one and two. To maintain his $50,000 withdrawal, he sells shares during the downturn. When the market eventually recovers, Robert will have far fewer shares to participate in that recovery. His portfolio never fully bounces back, and he runs out of money years before Margaret, despite the fact that over the full 30-year period, they experienced the same average annual return.

Robert's Portfolio (June 1999 – June 2014). Hypothetical portfolio beginning at $1,000,000 with $50,000 in annual withdrawals, allocated 60% S&P 500 (^SPX) and 40% Bloomberg U.S. Aggregate Bond Index (^BBUSATR). For illustrative purposes only. Indices are unmanaged and cannot be invested in directly. Past performance does not guarantee future results.

Same average. Wildly different outcomes. The only difference was timing.

What makes sequence risk particularly difficult to manage is that it's hard to see until it's too late. You won't know in advance whether you're retiring into a Margaret market or a Robert market. And the consequences of getting it wrong compound over time.

You cannot stop a 30% drop in the market. That's like standing in Gulfport Harbor and trying to stop a hurricane. It's not happening. Timing the market and going to cash may feel like the right decision, but in reality, you're adding more risk to your portfolio. In theory, you could time the market perfectly from top to bottom, but the odds are slim. And even the professionals rarely get it right. The best way to increase your odds is to create a retirement spending plan.

Planning Overcomes Sequence of Returns Risk

The good news: A retirement spending plan is the highest-impact move you can make to mitigate sequence of returns risk. Focusing on withdrawal rates, withdrawal order, and the tax implications of withdrawals can help your retirement plan work through unpredictable markets.

Market performance is out of your control. A spending plan is controllable. A spending plan accounts for best and worst-case scenarios, so you are prepared for whatever the market throws at you. It requires intention, but there are well-established strategies worth understanding before you build one.

Flexible Withdrawal Strategies

One of the most effective responses to sequence risk is not treating your withdrawal rate as fixed. A rigid withdrawal strategy, one that takes the same dollar amount from the portfolio regardless of market conditions, is the approach most vulnerable to bad market returns. A flexible approach adjusts withdrawals downward during periods of poor performance, reducing the number of shares sold at depressed prices.

Even modest flexibility (reducing spending by 10–15% in down years) can meaningfully extend portfolio longevity.

You're not cutting expenses to the bone. Maybe you're visiting the kids instead of traveling abroad. It could mean delaying a major purchase, and you're still living comfortably. And when the market is up, you do the opposite.

Research shows that adjusting spending in line with market performance can significantly increase your probability of success in retirement, especially for those with little guaranteed income from pensions or Social Security.

Cash Reserves and Bucket Strategies

Another consideration is maintaining a short-term cash reserve, a "cash bucket," that covers one to three years of living expenses. When markets are down, you draw from this reserve rather than selling investments at a loss. This buffer gives your portfolio time to recover before you need to sell.

The bucket approach separates your assets into time horizons:

- Cash for near-term needs

- Bonds for mid-term needs

- Stocks for longer-term growth

The psychological value shouldn't be underestimated. Knowing you have near-term income that doesn't depend on market performance can make it far easier to stay the course during a downturn.

Holding too much cash hurts your purchasing power over time. Holding too little exposes you to sequence of returns risk. For most retirees, the right balance falls between one and three years of living expenses.

Asset Allocation and Diversification

Your investment mix, often called asset allocation, is the main driver of risk and return in a portfolio. A portfolio heavily concentrated in stocks is more exposed to sharp short-term declines. A thoughtfully diversified portfolio (one that includes different asset classes with different return patterns) can reduce the magnitude of early losses without entirely sacrificing long-term growth potential.

Asset allocation isn't something you set once and forget. It should evolve as you move through retirement. Early on, your portfolio is balancing growth with preservation. You're drawing income and managing sequence risk at the same time. But as you age, your spending typically decreases, and your focus shifts from funding your own lifestyle to funding a legacy for your children or grandchildren. That shift extends your effective time horizon. And a longer time horizon, even in later retirement, can support a more growth-oriented allocation than you might expect.

The right allocation depends on your specific circumstances, time horizon, and income needs, which is why this conversation is best had with a fiduciary advisor who understands your full financial picture.

Reading the Market Environment

One thing a good financial planner can do is assess the current economic environment. While no one can predict the future, a good planner can tell you clearly what's happening in the economy today, and use that context to inform your investment strategy.

Markets move in cycles. The economy expands, peaks, contracts, and recovers. Understanding where we are in that cycle can help guide decisions about how your portfolio is positioned. Certain investments have historically performed better in different parts of the cycle, and aligning a portion of your portfolio accordingly can capture some upside when conditions are favorable and help cushion the downside when they're not.

This isn't market timing in the traditional sense. Changing your mix of stocks, bonds, and cash based on your economic outlook can be risky. Not always does the economy do what we think it will do. However, aligning a portion of your stocks in accordance with where we are in the economic cycle can provide upside when the market is performing well and mitigate downside when the economy performs poorly, which is significantly less risky than timing into cash. At Voyage, our satellite sleeve accomplishes this objective.

One additional tool worth knowing: the CAPE ratio. It measures whether the stock market appears expensive or cheap relative to corporate earnings over the past ten years, adjusted for inflation. When the CAPE ratio is high, stocks may be overvalued, meaning future returns could be more modest. When it's low, stocks may be undervalued, and the outlook more favorable. It's not a crystal ball, but for retirement plans with significant stock exposure, it's a useful data point when assessing what lies ahead.

Strategic Tax Planning

Sequence of returns risk also has a tax dimension that's easy to overlook. How you draw down your accounts, and which accounts you tap first (taxable, tax-deferred, tax-free), can have significant effects on both your tax liability and the longevity of your portfolio.

In a down market year, a Roth conversion may be worth considering, as you'd be converting at lower account values. The tax implications of withdrawal strategies are complex and individual. It's best to consult your financial professional and CPA before making any decisions.

Guaranteed Income Sources

Social Security, pensions, and certain annuity products can serve as a foundation of guaranteed income in retirement, income that doesn't require selling investments when markets are down. The more of your fixed expenses covered by guaranteed income, the less dependent your lifestyle is on portfolio performance in any given year. This reduces your effective exposure to sequence risk because your withdrawals from the investment portfolio become more discretionary.

When to claim Social Security is one of the most consequential decisions in a retirement plan, with long-term implications for total lifetime income. Consult your financial advisor on the timing that makes sense for your situation.

If you're considering an annuity, proceed carefully. ANNUITIES ARE SOLD - NOT BOUGHT. Commissions towards advisors can run as high as 10% of the money you put in. In my years, I've seen them over-recommended by advisors out to earn a commission. As a result, retirees have significantly less legacy dollars. They can't get their money when they need it. They don't understand the opaque and complex contract language the insurance company drew up. And they felt misled regarding how payouts are calculated.

It's the "easy button" to overcome market risk, but it comes at a cost. That's the trade-off you make with the insurance company to guarantee your income.

Annuities aren't inherently bad. Like any other financial product, they're a tool. Annuities have upsides and downsides. At Voyage, we may recommend an annuity if it helps strengthen your plan, but we do not earn commissions on that recommendation. We have no financial incentive to steer you in that direction. More often than not, the strategies above can strengthen your plan without locking you into a product you could regret down the road.

You Can't Control the Market. You Can Control the Plan.

The years surrounding your retirement date form what researchers sometimes call the "retirement danger zone," the window when your portfolio is most vulnerable to poor returns.

Understanding this risk is the first step. Building a financial plan that actively addresses it is what separates a retirement that holds together from one that doesn't.

At Voyage, our work with clients transitioning into retirement always includes an honest conversation about sequence risk: what it is, how their plan accounts for it, and what flexibility exists if markets move against them early. That kind of planning requires an advisor who understands your full picture, isn't motivated by product commissions, and is willing to build a strategy with you rather than sell you one. As one of the few fee-only fiduciaries on the Mississippi Gulf Coast, that's exactly how we work.

If you're within five to ten years of retirement and haven't specifically addressed sequence of returns risk, now is the time to do so. The market will not wait for you to schedule a meeting.

Key Questions Answered

What is sequence of returns risk in retirement?

Sequence of returns risk refers to the danger of experiencing significant investment losses in the early years of retirement. Unlike losses during your working years, when your paycheck covers living expenses, a market decline early in retirement forces you to sell investments at depressed prices to fund withdrawals. Once those shares are sold, they cannot recover with the market. The result is a smaller portfolio that must sustain the same level of income for the rest of retirement, often for decades.

Why does the timing of market losses matter more than their size?

Two retirees with identical average returns over 30 years can have vastly different outcomes depending on when losses occur. A retiree who experiences strong early returns, with poor returns coming later, can finish retirement with a significantly larger portfolio than one who experiences poor returns first, even if both average the same annual return. The reason is that early losses reduce the base from which future growth can compound, while early withdrawals lock in those losses permanently.

How can retirees protect against sequence of returns risk?

The most effective strategy is a retirement spending plan: a documented approach to withdrawal rates, account sequencing, and tax efficiency. Specific tools include flexible withdrawal strategies that reduce spending modestly in down years, a cash reserve (or "bucket") of one to three years of expenses to avoid selling during declines, a thoughtfully diversified asset allocation that evolves over time, and guaranteed income sources like Social Security that reduce dependence on portfolio distributions. The goal is to build a plan that holds up regardless of when a downturn arrives.

This content is for educational purposes only and is not intended as investment, tax, or legal advice. Nothing contained herein constitutes a recommendation or solicitation to buy or sell any security or investment strategy. Advisory services are offered through Voyage Wealth Management, LLC, an investment adviser registered with the state of Mississippi. Registration does not imply a certain level of skill or training. Past performance does not guarantee future results. All investing involves risk, including the potential loss of principal. The strategies discussed are for educational consideration only and may not be suitable for all investors. Please consult your tax advisor and financial professional regarding any strategies discussed herein, including Roth conversions and withdrawal sequencing.